Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Past Recessions Tell Us About the Housing Market

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

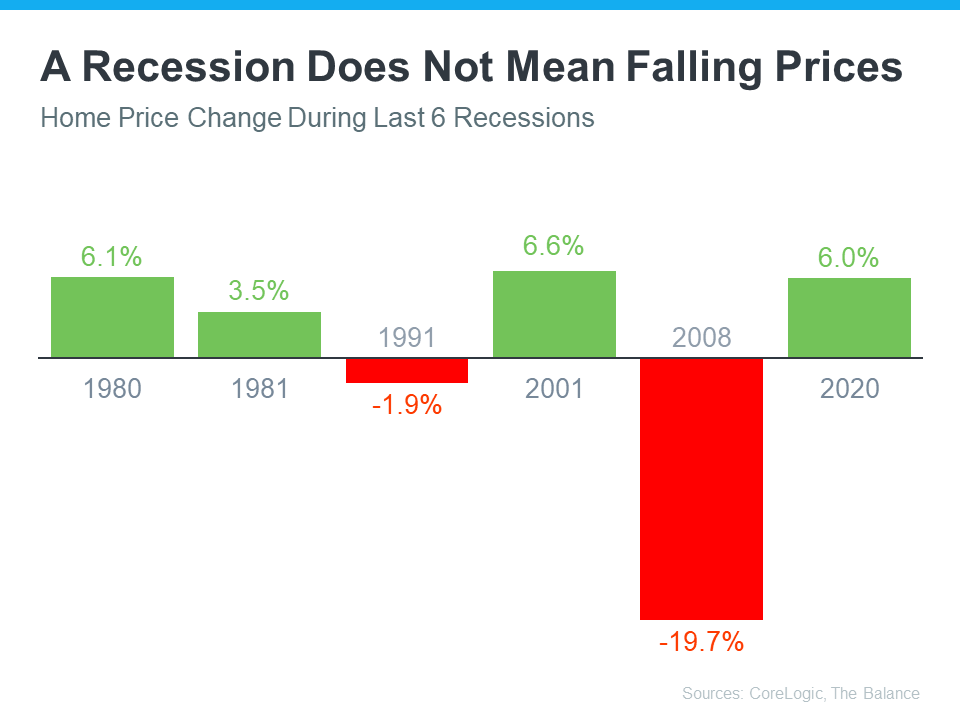

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

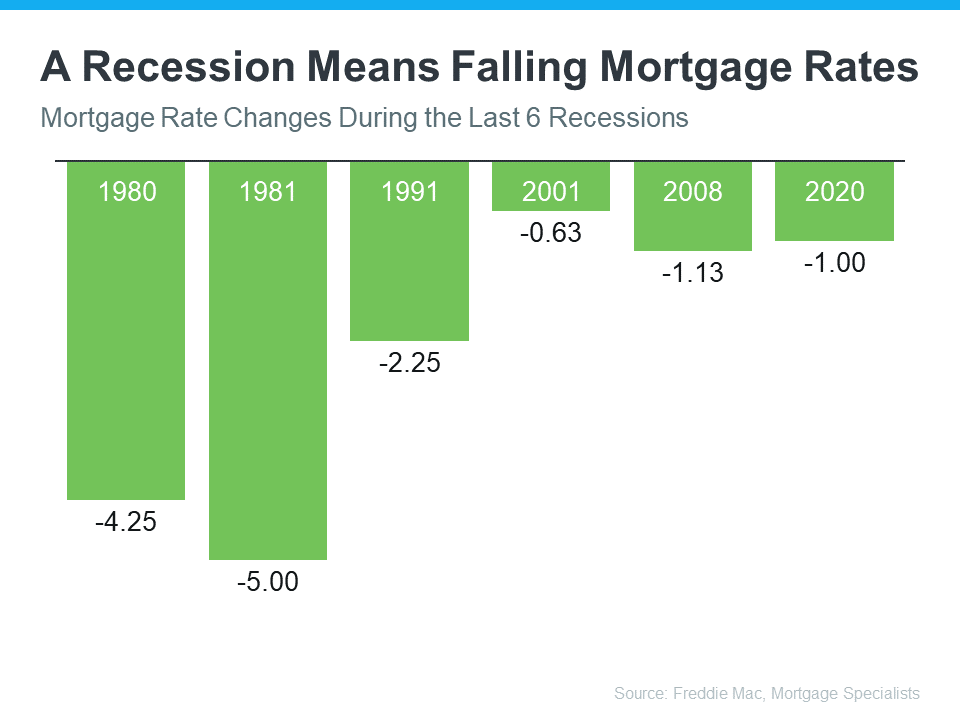

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

Bottom Line

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Is It Time To Sell Your Second Home?

During the pandemic, second homes became popular because of the rise in work-from-home flexibility. That’s because owning a second home, especially in the luxury market, allowed those homeowners to spend more time in their favorite places or with different home features. Keep in mind, a luxury home isn’t only defined by price. In a recent article, Investopedia shares additional factors that push a home into this category: location, such as a home on the water or in a desirable city, and features, the things that make the home itself feel luxurious.

A recent report from the Institute for Luxury Home Marketing (ILHM) explains just how much remote work impacted the demand for second and luxury homes:

“The unprecedented ten-fold increase towards remote work since the pandemic is an historic development that will continue to fuel second home demand for many years to come.”

But what if you bought a second home that you no longer use? If you’re now shifting back into the office or are seeing your priorities and needs change, you may find you’re not utilizing your second home as much. If so, it may be time to sell it.

And if you own what’s considered a luxury home, buyer demand for it may be even greater. In another report, the Institute for Luxury Home Marketing explains:

“. . . the last few years have left their legacy for the luxury market. While it might only represent a small percentage of the overall real estate market, luxury homeownership’s influence is growing. Not only has the purchase of homes valued over $1 million (a figure considered by the National Association of Realtors to be a benchmark for luxury) tripled from 2.6% to 6.5% since 2018, but demand for multiple luxury properties has soared over the last two years.

This phenomenal increase has been driven by a growing affluent demographic who consider owning a luxury property a necessity in their asset portfolio. All indications are that this trend is here to stay, albeit that demand is set to return to a more sustainable level.”

If you own a luxury second home that isn’t being used as much anymore, now’s the time to sell. There are still buyers in the market who are looking for a home like yours today.

Bottom Line

Let’s connect to explore the benefits of selling your second home this year.

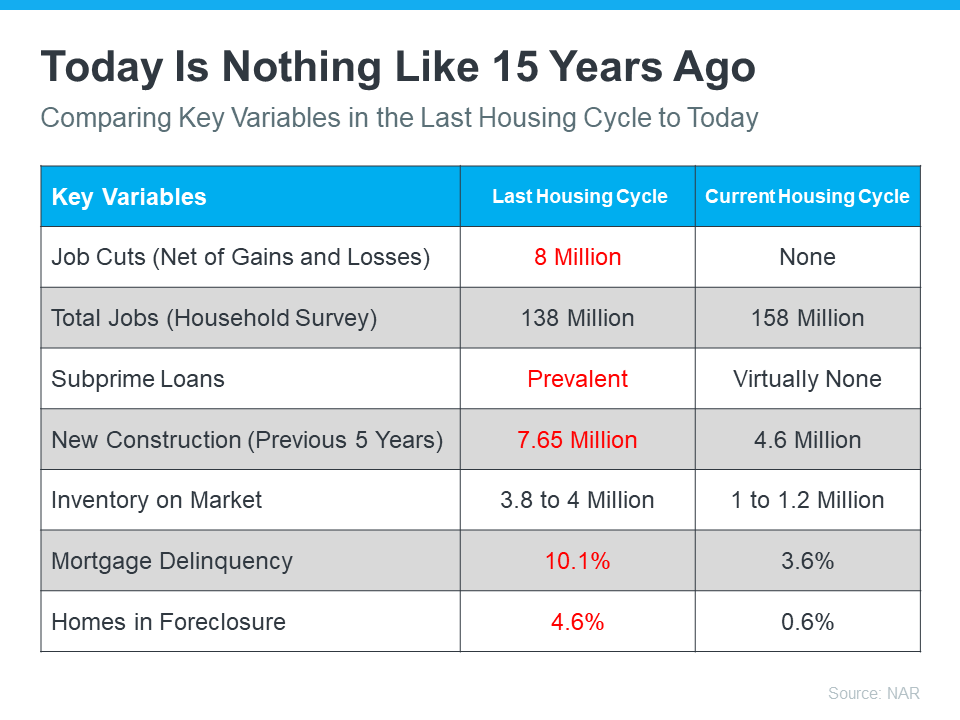

Today’s Housing Market Is Nothing Like 15 Years Ago

There’s no doubt today’s housing market is very different than the frenzied one from the past couple of years. In the second half of 2022, there was a dramatic shift in real estate, and it caused many people to make comparisons to the 2008 housing crisis. While there may be a few similarities, when looking at key variables now compared to the last housing cycle, there are significant differences.

In the latest Real Estate Forecast Summit, Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), drew the comparisons below between today’s housing market and the previous cycle:

Looking at the facts, it’s clear: today is very different than the housing market of 15 years ago.

There’s Opportunity in Real Estate Today

And in today’s market, with inventory rising and less competition from other buyers, there’s opportunity right now. According to David Stevens, former Assistant Secretary of Housing:

“So be advised…this may be the one and only window for the next few years to get into a buyer’s market. And remember…as the Federal Reserve data shows…home prices only go up and always recover from recessions no matter how mild or severe. Long term homeowners should view this market…right now…as a unique buying opportunity.”

Bottom Line

Today’s housing market is nothing like the real estate market 15 years ago. If you’re a buyer right now, this may be the chance you’ve been waiting for.

Why There Won’t Be a Flood of Foreclosures Coming to the Housing Market

With the rapid shift that’s happened in the housing market this year, some people are raising concerns that we’re destined for a repeat of the crash we saw in 2008. But in truth, there are many key differences between what’s happening today and the bubble in the early 2000s.

One of the reasons this isn’t like the last time is the number of foreclosures in the market is much lower now. Here’s a look at why there won’t be a wave of foreclosures flooding the market.

Not as Many Homeowners Are in Trouble This Time

After the last housing crash, over nine million households lost their homes due to a foreclosure, short sale, or because they gave it back to the bank. This was, in large part, because of more relaxed lending standards where people could take out mortgages they ultimately couldn’t afford. Those lending practices led to a wave of distressed properties which made their way into the market and caused home values to plummet.

But today, revised lending standards have led to more qualified buyers. As a result, there are fewer homeowners who are behind on their mortgages. As Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association (MBA), says:

“For the second quarter in a row, the mortgage delinquency rate fell to its lowest level since MBA’s survey began in 1979 – declining to 3.45%. Foreclosure starts and loans in the process of foreclosure also dropped in the third quarter to levels further below their historical averages.”

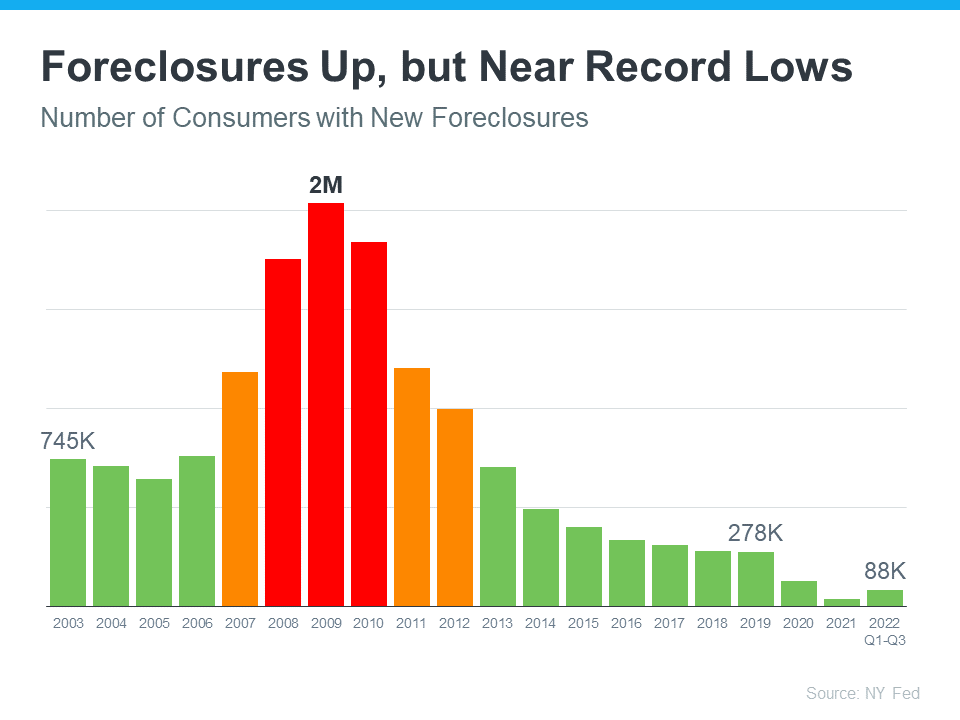

There Have Been Fewer Foreclosures over the Last Two Years

While you may have seen recent stories about the number of foreclosures rising today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The program gave homeowners facing difficulties extra time to get their finances in order and, in many cases, work out a plan with their lender.

With that program, many were concerned it would result in a wave of foreclosures coming to the market. That fear didn’t materialize. Data from the New York Fed shows there are still fewer foreclosures happening today than before the pandemic (see graph below):

That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019.

And most importantly, the number we’re seeing now is still far below the number we saw during the market crash (shown in the red bars in the graph). The big takeaway? Don’t let a headline in the news mislead you. While foreclosures are up year-over-year, historical context is essential to understanding the full picture.

Most Homeowners Have More Than Enough Equity To Sell Their Homes

Many homeowners today have enough equity to sell their homes instead of facing foreclosure. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home. And if they’ve stayed in their homes even longer, they may have even more equity than they realize. As Ksenia Potapov, Economist at First American, says:

“Homeowners have very high levels of tappable home equity today, providing a cushion to withstand potential price declines, but also preventing housing distress from turning into a foreclosure. . . the result will likely be more of a foreclosure ‘trickle’ than a ‘tsunami.’”

A recent report from ATTOM Data explains it by going even deeper into the numbers:

“Only about 214,800 homeowners were facing possible foreclosure in the second quarter of 2022, or just four-tenths of one percent of the 58.2 million outstanding mortgages in the U.S. Of those facing foreclosure, about 195,400, or 91 percent, had at least some equity built up in their homes.”

Bottom Line

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years. If you have questions, let’s connect.

3 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the average borrower with a home loan has almost $300,000 in equity right now.

As you weigh your options, especially in the face of inflation and talk of a recession, it’s important to understand your assets and how you can leverage them. A real estate professional is the best resource to help you understand how much home equity you have and advise you on some of the ways you can use it. Here are a few examples.

1. Buy a Home That Fits Your Needs

If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle.

If you want to upgrade your house, you can put your equity toward a down payment on the home of your dreams. And if you’re planning to downsize, you may be surprised that your equity may cover some, if not all, of the cost of your next home. A real estate advisor can help you figure out how much equity you have and how you can use it toward the purchase of your next home.

2. Reinvest in Your Current House

According to a recent survey from Point, 39% of homeowners would invest in home improvement projects if they chose to access their equity. This is a great option if you want to change some things about your living space but you aren’t ready to make a move just yet.

Home improvement projects allow you to customize your home to suit your needs and sense of style. Just remember to think ahead with any updates you make, as some renovations add more value to your home and are more likely to appeal to future buyers than others. For example, a report from the National Association of Realtors (NAR) shows refinishing or replacing wood flooring has a high cost recovery. Lean on a local professional for the best advice on which projects to invest in to get the greatest return on your investment when you sell.

3. Pursue Your Personal Goals

In addition to making a move or updating your house, home equity can also help you achieve the life goals you’ve dreamed of. That could mean investing in a new business venture, retiring or downsizing, or funding an education. While you shouldn’t use your equity for unnecessary spending, leveraging it to start a business or putting it toward education costs can help you achieve other lifelong goals.

Bottom Line

Your equity can be a game changer. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

Your House Could Be the #1 Item on a Homebuyer’s Wish List During the Holidays

Each year, homeowners planning to make a move are faced with a decision: sell their house during the holidays or wait. And others who have already listed their homes may think about removing their listings and waiting until the new year to go back on the market.

The truth is many buyers want to purchase a home for the holidays, and your house might be just what they’re looking for. Here are five great reasons you shouldn’t wait to sell your house.

1. While the supply of homes for sale has increased this year, there still aren’t enough homes on the market to keep up with buyer demand. As Nadia Evangelou, Senior Economist & Director of Forecasting at the National Association of Realtors (NAR), explains:

“There’s still this gap between demand and supply because we were underbuilding for many years. . . . So now we see demand is slowing, but it still outpaces supply.”

2. Serious homebuyers are out looking right now. Millennials are driving homebuying demand today, and many are eager to make a purchase. Mark Fleming, Chief Economist at First American, explains:

“While not the frenzy of 2021, the largest living generation, the Millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market.”

3. The desire to own a home doesn’t stop during the holidays. In fact, homes decorated for the holidays appeal to many buyers. Plus, purchasers who look for homes during the holidays are ready to buy.

4. You can restrict the showings in your house to days and times that are most convenient for you. That can help you minimize disruptions, which is especially important this time of year.

5. Rents have skyrocketed in recent years. And, many buyers are looking to escape rising rents and avoid falling into the rental trap for another year. As an article from Zillow says:

“Over the next 12 months, rents are expected to grow more than inflation, the stock market and home values.”

Your home could be their ticket to leaving renting behind for good.

Bottom Line

There are still many reasons it makes sense to list your house during the holiday season. Let’s connect to determine if selling now is your best move.

Home Equity: A Source of Strength for Homeowners Today

Experts agree there’s no chance of a large-scale foreclosure crisis like we saw back in 2008, and that’s good news for the housing market. As Mark Fleming, Chief Economist at First American, says:

“. . . don’t expect a housing bust like the mid-2000s, as lending standards in this housing cycle have been much tighter and homeowners have historically high levels of home equity, so there likely won’t be a surge in foreclosures.”

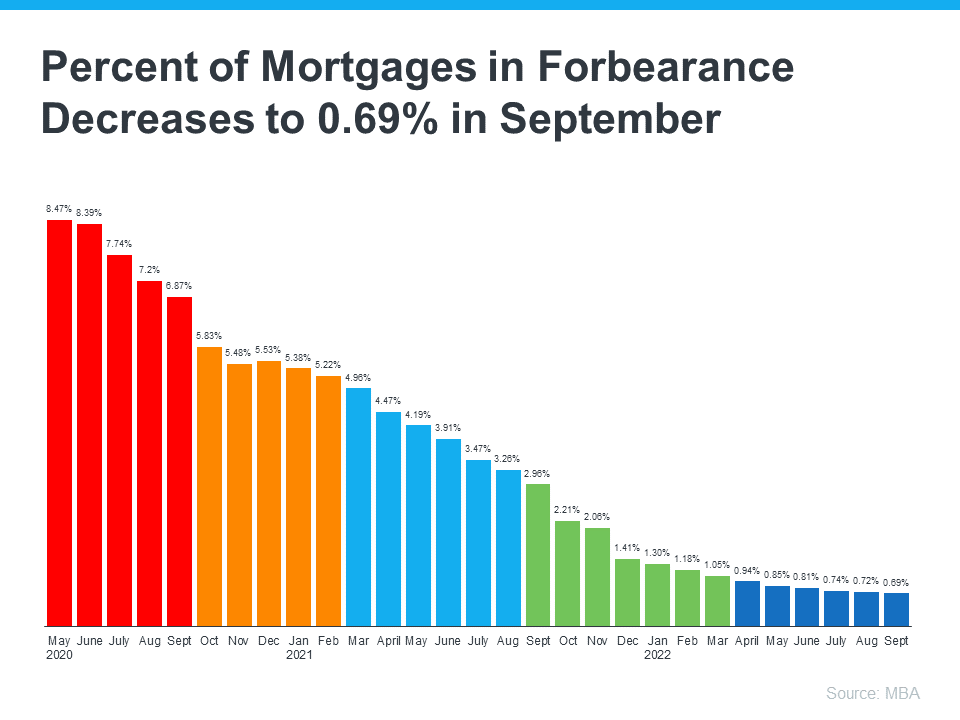

Data from the Mortgage Bankers Association (MBA) helps tell this story. It shows the overall percentage of homeowners at risk is decreasing significantly with time (see graph below):

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

But even though the volume of homeowners at risk is very low, there is still a small percentage of homeowners who may be coming face to face with foreclosure as a possibility today. If you’re facing difficulties yourself, it can help to understand your options. It starts with knowing what foreclosure is. Investopedia defines it like this:

“Typically, default is triggered when a borrower misses a specific number of monthly payments . . . Foreclosure is the legal process by which a lender attempts to recover the amount owed on a defaulted loan by taking ownership of and selling the mortgaged property.”

The good news is there are alternatives available to help you avoid going through the foreclosure process, including:

- Reinstatement

- Loan modification

- Deed-in-lieu of foreclosure

- Short sale

But before you go down any of those paths, it’s worth seeing if you have enough equity in your home to sell it and protect your investment.

You May Be Able To Use Your Equity To Sell Your House

Equity is the difference between what you owe on the home and its market value based on factors like price appreciation.

In today’s real estate market, many homeowners have far more equity in their homes than they realize due to the home price appreciation we’ve seen over the past few years. According to CoreLogic:

“The total average equity per borrower has now reached almost $300,000, the highest in the data series.”

So, what does that mean for you? If you’ve lived in your house for at least a few years or more, chances are your home’s value, and your equity, has risen dramatically. In addition, the mortgage payments you’ve made during that time chipped away at the balance of your loan. If your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage.

Rick Sharga, Executive VP of Market Intelligence at ATTOM Data, explains how equity can help:

“Very few of the properties entering the foreclosure process have reverted to the lender at the end of the foreclosure. . . We believe that this may be an indication that borrowers are leveraging their equity and selling their homes rather than risking the loss of their equity in a foreclosure auction.”

Lean on Experts To Explore Your Options

To find out how much equity you have, work with a local real estate professional. They can give you an estimate of what your house could sell for based on recent sales of similar homes in your area. You may be able to sell your house to avoid foreclosure.

If you find out you have to pursue other options, your agent can help with that too. They’ll be able to connect you with other professionals in the industry, like housing counselors, who can look into your unique situation and offer advice on next steps if selling isn’t your best alternative.

Bottom Line

If you’re a homeowner facing hardship, let’s connect so you have an expert on your side to explore your options and see if you can sell your house to avoid foreclosure.

Key Factors Affecting Home Affordability Today

Every time there’s a news segment about the housing market, we hear about the affordability challenges buyers are facing today. Those headlines are focused on how much mortgage rates have climbed this year. And while it’s true rates have risen dramatically, it’s important to remember they aren’t the only factor in the affordability equation.

Here are three measures used to establish home affordability: home prices, mortgage rates, and wages. Let’s look closely at each one.

1. Mortgage Rates

This is the factor most people are focused on when they talk about homebuying conditions today. So far, current rates are almost four full percentage points higher than they were at the beginning of the year. As Len Kiefer, Deputy Chief Economist at Freddie Mac, explains:

“U.S. 30-year fixed mortgage rates have increased 3.83 percentage points since the end of last year. That’s the biggest year-to-date increase in rates in over 50 years.”

That increase in mortgage rates is impacting how much it costs to finance a home purchase, creating a challenge for many buyers that’s pricing some out of the market. While the current global uncertainty makes it difficult to project where mortgage rates will go in the future, experts do say that rates will likely remain high as long as inflation does.

2. Home Prices

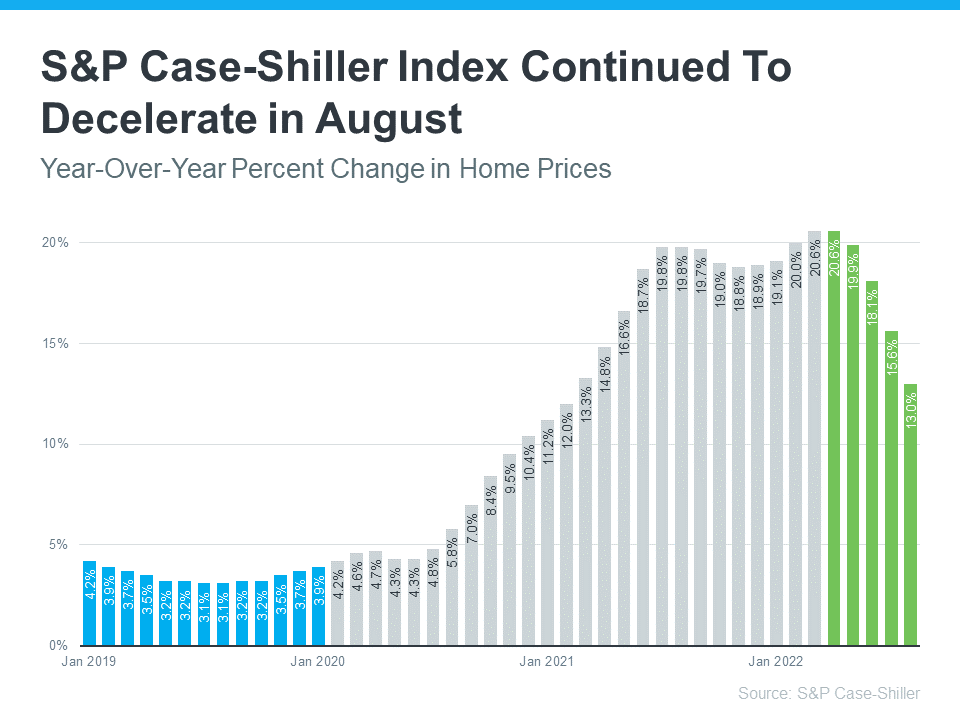

The second factor at play is home prices. Home prices have made headlines over the past few years because they skyrocketed during the pandemic. Now, the most recent Home Price Index from S&P Case-Shiller shows home values continued to decelerate for a fifth consecutive month (shown in green in the graph below):

This deceleration is happening because higher mortgage rates are moderating demand, and as a result, easing the buyer competition and bidding wars that previously drove prices up.

What’s worth noting though, is how much higher home prices still are than they were before the pandemic (shown in blue in the graph above). Even now, we have a long way to go to get to more normal levels of home price appreciation, which is historically closer to 4%. When both mortgage rates and home prices are high, affordability and your purchasing power become a greater challenge.

But while prices are still elevated in many markets, some areas are seeing slight declines. It all depends on your local market. For insight into what’s happening in your area, reach out to a trusted real estate professional.

3. Wages

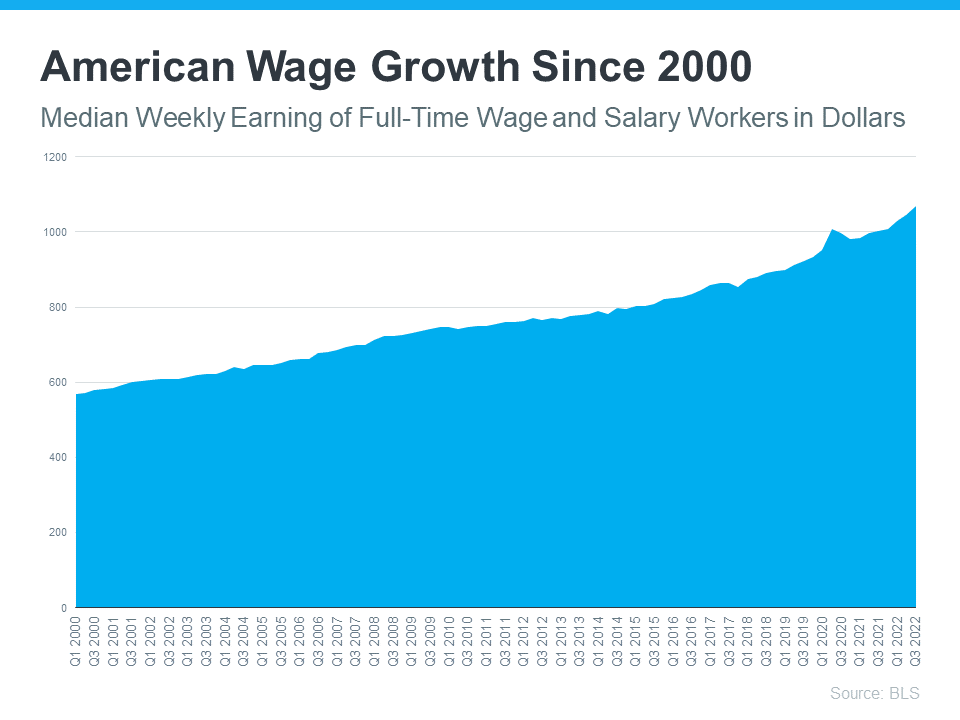

The one big, positive component in the affordability equation is the increase in American wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have grown over time. This year is no exception.

As the Bureau of Labor Statistics (BLS) reports:

“Median weekly earnings of the nation’s 120.2 million full-time wage and salary workers were $1,070 in the third quarter of 2022 (not seasonally adjusted), the U.S. Bureau of Labor Statistics reported…This was 6.9 percent higher than a year earlier…”

So, when you think about affordability, remember the full picture includes more than just mortgage rates. Home prices and wages need to be factored in as well. Because wages have been rising, they’re a big reason why serious buyers are still purchasing homes this year.

If you have questions or want to learn more, reach out to a trusted advisor who can explain how all of these variables work together and what’s happening in your area. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

“Buying or selling a home involves a series of requirements and variables, and it’s important to have someone in your corner from start to finish to make the process as smooth as possible… and objectivity to deliver trusted expertise to consumers in every U.S. ZIP code.”

Bottom Line

To learn more, let’s connect today and make sure you have a trusted lender so you’re able to make an informed decision if you’re planning to buy or sell a home right now.

The Majority of Americans Still View Homeownership as the American Dream

Buying a home is a powerful decision, and it remains a key part of the American Dream. In fact, the 2022 Consumer Insights Report from Mynd found the majority of people polled still view homeownership as a key life achievement. Let’s explore just a few of the reasons why so many Americans continue to value homeownership.

The Financial Benefits of Owning a Home

One possible reason homeownership is viewed so highly is because owning a home is a significant wealth-building tool, and it provides meaningful financial stability over renting by locking in your monthly housing payments for the length of your home loan. An article from Forbes explains:

“Understanding the potential benefits of homeownership helps individuals see the value of owning property instead of renting. . . . household wealth among homeowners is a whopping 1,469% higher on average compared to renters, excluding home equity, making the allure of homeownership even more enticing.”

Over time, owning a home not only helps boost your own net worth, but it also sets future generations up for success as you pass that wealth down. That may be why the Mynd report also says:

“Most Americans (78%) still associate homeownership with the ‘American dream.’ And nearly two-thirds of Americans (65%) see homeownership as a means of building intergenerational wealth.”

The Non-Financial Benefits of Homeownership

While the financial benefits of owning a home are important, becoming a homeowner impacts you on a social and emotional level, too. As Mark Fleming, Chief Economist for First American, says:

“. . . buying a home is not just a financial decision. It’s also a lifestyle decision.”

Your home provides feelings of achievement, responsibility, and more. 3by30 highlights the top 10 benefits homeowners enjoy. A few non-financial advantages include:

- Providing you with more freedom and control over your living space

- Giving you a greater sense of pride

- Helps with community engagement

What Does That Mean for You?

If your definition of the American Dream involves greater freedom and prosperity, then homeownership could play a major role in helping you achieve that dream. While it may feel challenging to buy a home today as mortgage rates and home prices rise, if the time is right for you, know that there are incredible benefits waiting for you at the end of your journey. You’ll have a place you can grow your wealth, call your own, and feel most comfortable.

Like the National Association of Realtors (NAR) says:

“. . . research has consistently shown that homeownership is also associated with multiple economic and social benefits to individual homeowners. Homeownership has always been an important way to build wealth.”

Bottom Line

Buying a home is a powerful decision and a key part of the long-term dream for many Americans. And if homeownership is part of your dreams this year, let’s connect to start the process today.

Sell Your House Before the Holidays

As you look ahead to the winter season, you’re likely making plans and thinking about what you want to achieve before the year ends. One of those key decision points could be whether or not you want to move this year. If the location or size of your current home no longer meets your needs, finding a house that better suits your lifestyle may be a top priority for you. But with today’s cooling housing market, is it really a good time to sell your house, or should you wait?

If you’re ready to make your decision, here are three reasons you may want to consider selling before the holidays.

1. Get One Step Ahead of Other Sellers

Typically, in the residential real estate market, homeowners are less likely to list their houses toward the end of the year. That’s because people get busy around the holidays and deprioritize selling their house until the start of the new year when their schedules and social calendars calm down.

Selling now, while other homeowners may hold off until after the holidays, can help your house stand out. Start the process with a real estate professional today so you can get your house on the market and get ahead of your competition.

2. Get in Front of Serious Buyers This Season

Even though housing supply has increased this year as buyer demand has moderated, it’s still low overall. That means there aren’t enough homes on the market today, especially as the millennial generation reaches their peak homebuying years. As Mark Fleming, Chief Economist at First American, says:

“While not the frenzy of 2021, the largest living generation, the Millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market.”

Serious buyers will still be looking this winter and your house may be exactly what they’re searching for. If you work with an agent to list your house now, you’ll be able to get in front of the eager buyers who are hoping to make a move before the year ends.

3. Seize a Great Chance To Move Up

Don’t forget, today’s homeowners have record amounts of equity. According to CoreLogic, the average amount of equity per mortgage holder has climbed to almost $300,000. That’s an all-time high. That means the equity you have in your house right now could cover some, if not all, of a down payment on the home of your dreams.

And as you weigh the reasons to sell before winter, don’t lose sight of why you’re thinking about moving in the first place. Maybe it’s time to buy a house that’s in a better location for you, has the space you and your loved ones have been craving, or simply gives you that sense of home. A trusted real estate advisor can help you determine how much home equity you have and how you can use it to achieve your goal of making a move.

Bottom Line

If you’re thinking about selling your house so you can find a home that better suits your needs, don’t delay your plans. Let’s connect so you can accomplish your goals before winter.