Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Pre Listing Home Inspections:

Mike drops by California Leasing to talk with John Evarts & Martin Rodriguez about the benefits of Pre Listing home inspections!

Coming Soon!!

***Beautiful, Upgraded Home In Castaic’s Popular, Stonegate Community!*** This newly remodeled two-bedroom, two-bathroom home has been professionally inspected, and is move-in ready! The home has an open floor plan, private location, mountain views, and lush landscaping. The living room is spacious with high ceilings, upgraded floors, and is open to the dining room. The dining room glass sliding door leads you outside to a private park-like setting with shady patio cover and custom outdoor bar. The kitchen is remodeled and freshly painted. It features custom a backsplash and flooring with an over-sized breakfast bar that opens to the dining room, making it great for entertaining! The master suite features high ceilings, a walk-in closet, and a sliding glass door leading to the covered backyard patio. The newly remodeled master bathroom is truly spectacular! Light, bright, and open, the custom skylight brings the sunshine inside and shows off the white porcelain marble tile! It features a separate shower and soaking tub. The vanity, fixtures, and porcelain are all new and upgraded! Access the two-car garage directly from inside the home, there you will find plenty of additional shelving. The home has great curb appeal and a wide driveway for additional parking. There is also additional guest parking close by. Located minutes from the freeway, it has award-winning schools, great shopping, dining, recreation, and Magic Mountain theme park all close by. The Stonegate HOA includes a pool, spa, clubhouse, fitness center, and RV parking!

Available For Lease October 01!

Available October 01, 2024!

Charming, centrally located, North Valencia Home. Near award winning schools, parks, public transportation, shops and restaurants! This will go fast!

Your Santa Clarita Valley Real Estate Update For July 2024

What You Should Know About Closing Costs

Before you buy a home, it’s important to plan ahead. While most buyers consider how much they need to save for a down payment, many are surprised by the closing costs they have to pay. To ensure you aren’t caught off guard when it’s time to close on your home, you need to understand what closing costs are and how much you should budget for.

What Are Closing Costs?

People are sometimes surprised by closing costs because they don’t know what they are. According to Bankrate:

“Closing costs are the fees and expenses you must pay before becoming the legal owner of a house, condo or townhome . . . Closing costs vary depending on the purchase price of the home and how it’s being financed . . .”

In other words, your closing costs are a collection of fees and payments involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

- Government recording costs

- Appraisal fees

- Credit report fees

- Lender origination fees

- Title services

- Tax service fees

- Survey fees

- Attorney fees

- Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical, too. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $366,900. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $7,500 and $18,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared at Closing Time?

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

Work with a team of trusted real estate professionals to understand exactly how much you’ll need to budget for closing costs. An agent can help connect you with a lender, and together your expert team can answer any questions you might have.

Bottom Line

It’s important to plan for the fees and payments you’ll be responsible for at closing. Let’s connect so I can help you feel confident throughout the process.

Why Today’s Housing Market Isn’t Headed for a Crash

67% of Americans say a housing market crash is imminent in the next three years. With all the talk in the media lately about shifts in the housing market, it makes sense why so many people feel this way. But there’s good news. Current data shows today’s market is nothing like it was before the housing crash in 2008.

Back Then, Mortgage Standards Were Less Strict

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance an existing one.

As a result, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

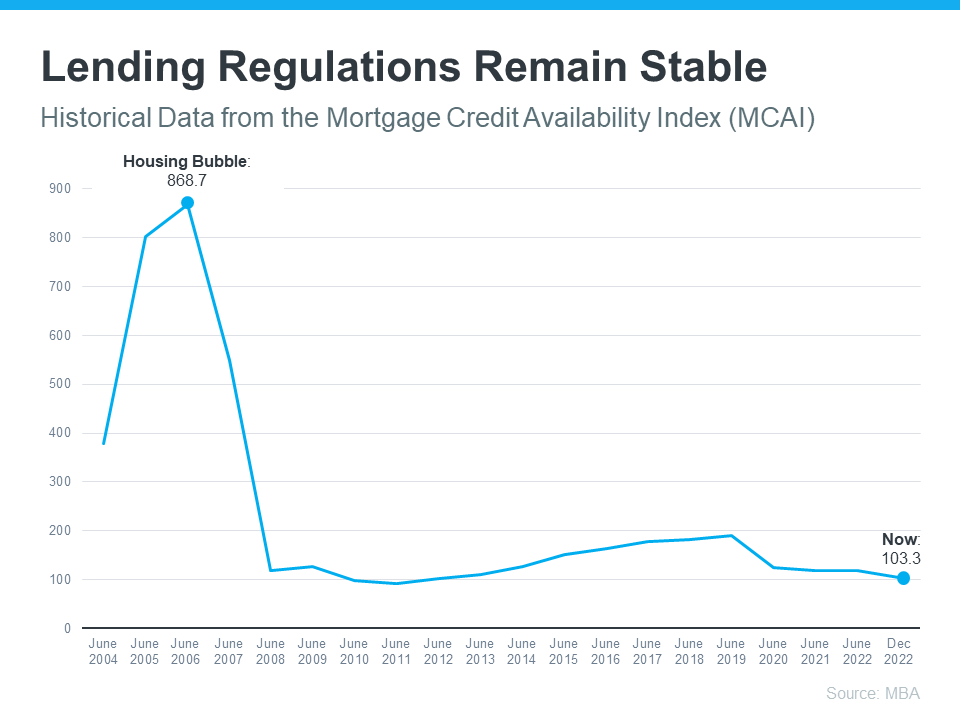

The graph below uses data from the Mortgage Bankers Association (MBA) to help tell this story. In this index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards have helped prevent a situation that could lead to a wave of foreclosures like the last time.

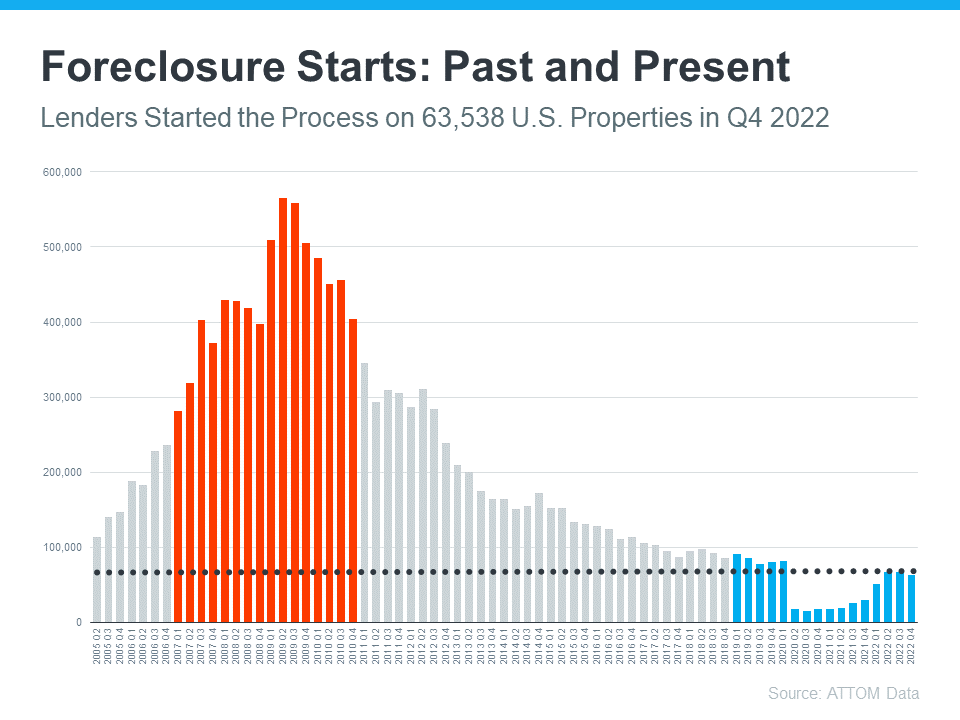

Foreclosure Volume Has Declined a Lot Since the Crash

Another difference is the number of homeowners that were facing foreclosure when the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM to show the difference between last time and now:

So even as foreclosures tick up, the total number is still very low. And on top of that, most experts don’t expect foreclosures to go up drastically like they did following the crash in 2008. Bill McBride, Founder of Calculated Risk, explains the impact a large increase in foreclosures had on home prices back then – and how that’s unlikely this time.

“The bottom line is there will be an increase in foreclosures over the next year (from record level lows), but there will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.”

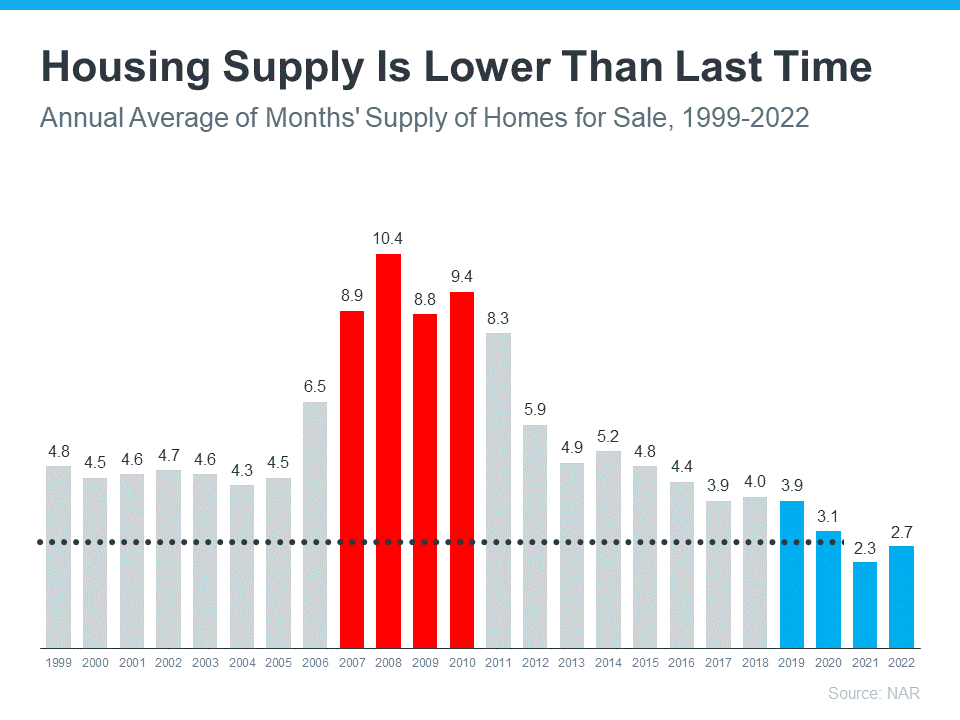

The Supply of Homes for Sale Today Is More Limited

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just 2.7-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

Bottom Line

If recent headlines have you worried we’re headed for another housing crash, the data above should help ease those fears. Expert insights and the most current data clearly show that today’s market is nothing like it was last time.

Number of Homes for Sale Up from Last Year, but Below Pre-Pandemic Years

The biggest challenge in the housing market right now, and likely for years to come, is how few homes there are for sale compared to the number of people who want to buy. That’s why, if you’re thinking about selling your house, this is a great time to do so. Your house would be welcome in a market that has fewer homes for sale than it did in the years leading up to the pandemic.

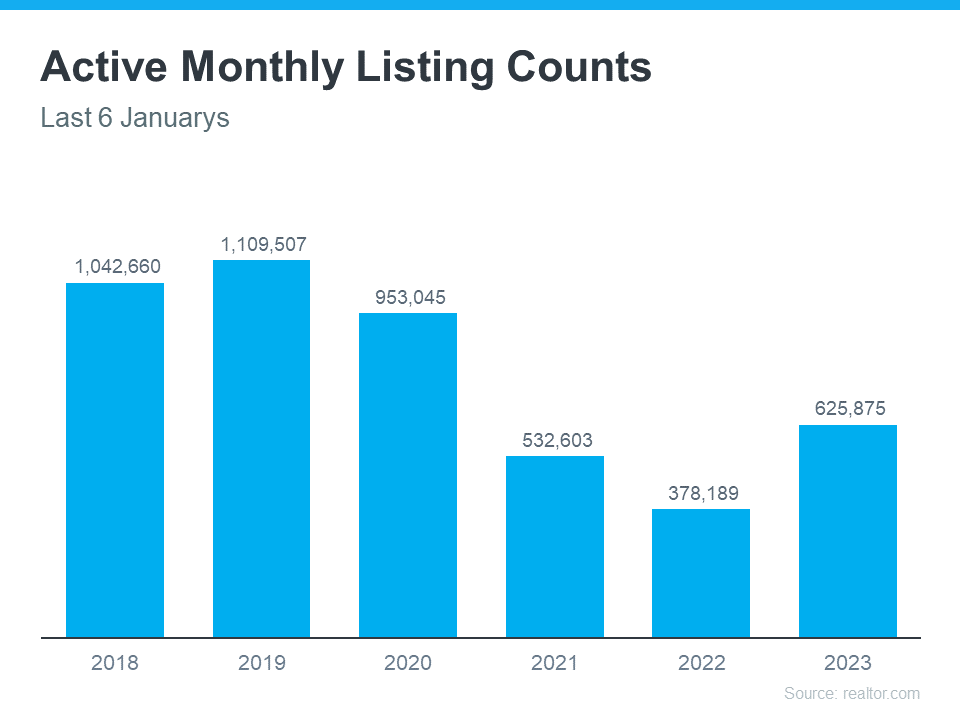

According to the latest Monthly Housing Market Trends Report from realtor.com:

“There were 65.5% more homes for sale in January compared to the same time in 2022. This means that there were 248,000 more homes available to buy this past month compared to one year ago. While the number of homes for sale is increasing, it is still 43.2% lower than it was before the pandemic in 2017 to 2019. This means that there are still fewer homes available to buy on a typical day than there were a few years ago.”

The graph below shows how today’s inventory of homes for sale compares to recent years:

What Does This Mean for You?

Fewer homes for sale means buyers have fewer choices than they did prior to the pandemic—and that frustration is leading some to give up on the homebuying process altogether. But with mortgage rates sitting lower than they were at the peak last fall, more buyers are willing to come back into the process—they just need to find homes to buy. This is welcome activity for the spring market, especially if you’re thinking of selling your house.

With a renewed interest in buying a home for many, the New York Times (NYT) reports:

“Home buyers are edging back into the market after being sidelined last year . . .”

So, if you want to take advantage of a sweet spot in the market, this spring could be your shot.

Bottom Line

The housing market needs more homes for sale to meet the demand of today’s buyers. If you’ve thought about selling, now’s the time for us to connect and get ready for you to make a move this spring.

Think Twice Before Waiting for 3% Mortgage Rates

Last year, the Federal Reserve took action to try to bring down inflation. In response to those efforts, mortgage rates jumped up rapidly from the record lows we saw in 2021, peaking at just over 7% last October. Hopeful buyers experienced a hit to their purchasing power as a result, and some decided to press pause on their plans.

Today, the rate of inflation is starting to drop. And as a result, mortgage rates have dipped below last year’s peak. Sam Khater, Chief Economist at Freddie Mac, shares:

“While mortgage market activity has significantly shrunk over the last year, inflationary pressures are easing and should lead to lower mortgage rates in 2023.”

That’s potentially great news if you’re a buyer aiming to jump back into the housing market. Any drop in mortgage rates helps boost your purchasing power by bringing down your expected monthly mortgage payment. This means the lower mortgage rates experts forecast this year could be just what you need to reignite your homebuying goals.

While this opens up a window of opportunity for you, remember: you shouldn’t expect rates to drop back down to record lows like we saw in 2021. Experts agree that’s not the range buyers should bank on. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“I think we could be surprised at how much mortgage rates pull back this year. But we’re not going back to 3 percent anytime soon, because inflation is not going back to 2 percent anytime soon.”

It’s important to have a realistic vision for what you can expect this year, and that’s where the advice of expert real estate advisors is critical. You may be surprised by the impact even a mild drop in mortgage rates has on your budget. If you’re ready to buy a home now, today’s market presents the opportunity to get a more affordable mortgage rate, find your dream home, and face less competition from other buyers.

Bottom Line

The recent pullback in mortgage rates is great news – but if you’re ready to buy now, holding out for 3% is a mistake. Work with a local lender to learn how today’s rates impact your goals, and let’s connect to explore your options in our area.